I have been asked lately if I have a guide of some type that would help educate first time buyers with regard to to all the things they should know about buying thier first home. With that in mind here is the first part of what will be a multiple series of blogs designed to tell you everything you need to know about buying and financing a home from A-Z. Since one of the biggest factors in obtaining mortgage financing is credit, let’s dive right in with information you need to know about credit, how credit scoring works and what you can do to correct errors in your credit report.

This Home Financing Guide is designed to provide information so that you can reach your home financing goals while avoiding mistakes along the way that can not only delay the process but can be costly as well. This guide will be broken down in several posts and I will try to keep it as comprehensive as possible. Check back for updates often as this may easily be a 7 or 8 part blog giving you the most comprehensive information you can find about purchasing and financing your new home. If you have any questions while reading the material, please feel free to call me any time.

Steve Fingerman

Branch Manager

Hernando County Mortgage Lender

4117 Mariner Blvd.

Hernando County Florida, 34609

Your credit is one of the key factors in your ability to obtain home financing. You may have heard many companies talk about credit, about how important it is and how you need to know what is on your credit report. They are absolutely right. Your credit not only determines whether you qualify for a home loan, it also determines costs such as interest rate on credit cards, premiums on auto insurance, and in fact it can be used to screen your employment. You credit is definitely important.

Credit is made up of several components all of which become part of your credit report.

- Applications for credit

- Number of open accounts credit accounts and account age (credit cards and loans)

- Accounts Balances

- Payment history (on-time or late)

- Collections, foreclosures, repossessions

- Bankruptcies, liens and other public records

- Past addresses, employers and names

- Your calculated credit score (FICO score)

A person that has a credit score below 620 will have a difficult time obtaining a mortgage loan. (There used to be a category of loans called Subprime but given the high risk and abuse that program is all but gone today). A credit score between 620 and 659 may need to select a government sponsored program to qualify. If the credit score is between 660-719 most loan programs become available. But at 720 and above the best interest rates and terms are available to those Borrowers.

Each of the three major credit bureaus will assign a credit score. When it comes to mortgage lending all three credit scores are used in the evaluation of credit with the middle score of the three being the determining factor. For example if a prospective borrower had scores of 719, 728 and 721, the 721 would be the determining score (the middle one). One other important factor to remember is that if you have a co-borrower (e.g. spouse) that the lower of your and all co-borrowers middle credit score will be the score used for loan qualification.

| 750 and up | Excellent |

| 720-749 | Good |

| 660-719 | Fair |

| 620-659 | Marginal |

| 619 and below | Poor |

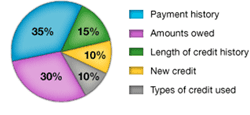

Of the various components that affect your credit score the one that has the most impact is payment history (making on-time payments). That is followed by your credit balances (how much you owe), and how long you have had established credit. The chart to the right shows the importance of each of these factors. However, it should be noted that if a person has a recent bankruptcy, foreclosure, or collection account, those kinds of situations will cause the credit score to drop sharply.

It is important that you review your credit report on a periodic basis. Often individuals find that there are errors and inaccuracies that are causing their credit report to look worse that it really should be. Sometimes credit entries are posted to the wrong account. You may also find collection accounts for medical bill that you thought your insurance had covered. There are some estimates that over 40% of all credit reports have one or more errors on them. But if you don’t look at your credit report, you would not know that they were there.

You can obtain your free credit report from http://annualcreditreport.com/. This website is sponsored by the big three credit bureaus: TransUnion, Experian and EquiFax. Do not go to other credit advertising websites such as FreeCreditReport.com unless you wish to buy additional services. On those websites you may be lulled into a free credit report but in order to receive it you have to sign up for a trial subscription to a service. You are allowed one free report from each of the major credit bureaus each year (up to 3 free reports). Given that it may be a good strategy to obtain a credit report from each credit bureau four (4) months apart and that way you are able to look at the report multiple times each year at no cost to you.

If you do find problems with your credit report, first contact the creditor (card issuer or loan holder) that the problem lies with. If you cannot get a satisfactory resolution with the creditor then contact each of the credit bureaus that shows the reported credit item in question and conduct a formal dispute by writing letters to the credit bureaus stating what the issue(s) is and requesting correction(s) to the credit report. The credit bureaus are pretty helpful when it comes to clearing up issues such as these. You have the right to an accurate credit report under the Fair and Accurate Credit Reporting Act. Anytime you get a positive response from the creditor be sure to ask for the confirmation of correction or removal in writing and keep that document for future reference.

For Additional Information about Credit and The impact it can have on your Mortgage please call me to discuss your needs in detail. I am available any time, and will do my best to give you the best information possible so that you can make sure we are securing the best possible terms on your first home.

Steve Fingerman

Branch Manager

Hernando County Mortgage Lender

Office 352-688-7949

Cell 727-946-0904